The Switzerland market closed higher on Friday, tracking positive cues from other European markets amid hopes the Federal Reserve will cut interest rates next week, and possibly announce more reductions before the end of the year. As investors navigate these favorable conditions, identifying high-growth tech stocks becomes crucial for capitalizing on potential market gains.

Top 10 High Growth Tech Companies In Switzerland

| Name | Revenue Growth | Earnings Growth | Growth Rating |

|---|---|---|---|

| LEM Holding | 8.69% | 18.38% | ★★★★☆☆ |

| ALSO Holding | 11.99% | 23.95% | ★★★★☆☆ |

| Santhera Pharmaceuticals Holding | 24.38% | 35.40% | ★★★★★★ |

| Comet Holding | 21.67% | 48.51% | ★★★★★★ |

| Temenos | 7.59% | 14.32% | ★★★★☆☆ |

| SoftwareONE Holding | 8.60% | 52.57% | ★★★★★☆ |

| Cicor Technologies | 7.10% | 27.73% | ★★★★☆☆ |

| Basilea Pharmaceutica | 8.99% | 36.39% | ★★★★★☆ |

| Sensirion Holding | 13.96% | 104.68% | ★★★★☆☆ |

| Kudelski | 9.93% | 120.15% | ★★★★☆☆ |

Let’s dive into some prime choices out of from the screener.

Simply Wall St Growth Rating: ★★★★☆☆

Overview: ALSO Holding AG operates as a technology services provider for the ICT industry in Switzerland, Germany, the Netherlands, Poland, and internationally with a market cap of CHF3.22 billion.

Operations: The company generates revenue primarily from Central Europe (€4.62 billion) and Northern/Eastern Europe (€5.24 billion). The total market cap stands at CHF3.22 billion, reflecting its significant presence in the ICT industry across multiple regions.

ALSO Holding AG, a notable player in the Swiss tech sector, reported half-year sales of €4.28 billion, down from €4.83 billion last year. Despite this 7.3% decline in sales, earnings are projected to grow at an impressive 24% annually over the next three years, outpacing the Swiss market’s forecast of 11.7%. With a focus on R&D expenses totaling €120 million (2.8% of revenue), ALSO is investing heavily in innovation to drive future growth and maintain its competitive edge in software and AI segments.

In addition to these investments, ALSO repurchased shares worth €50 million this year, reflecting confidence in its long-term prospects despite recent volatility. The company’s net income for H1 2024 was €41.66 million compared to last year’s €52.53 million; however, with expected annual revenue growth of 12%, it remains well-positioned within the industry context where SaaS models are becoming increasingly prevalent for recurring revenues.

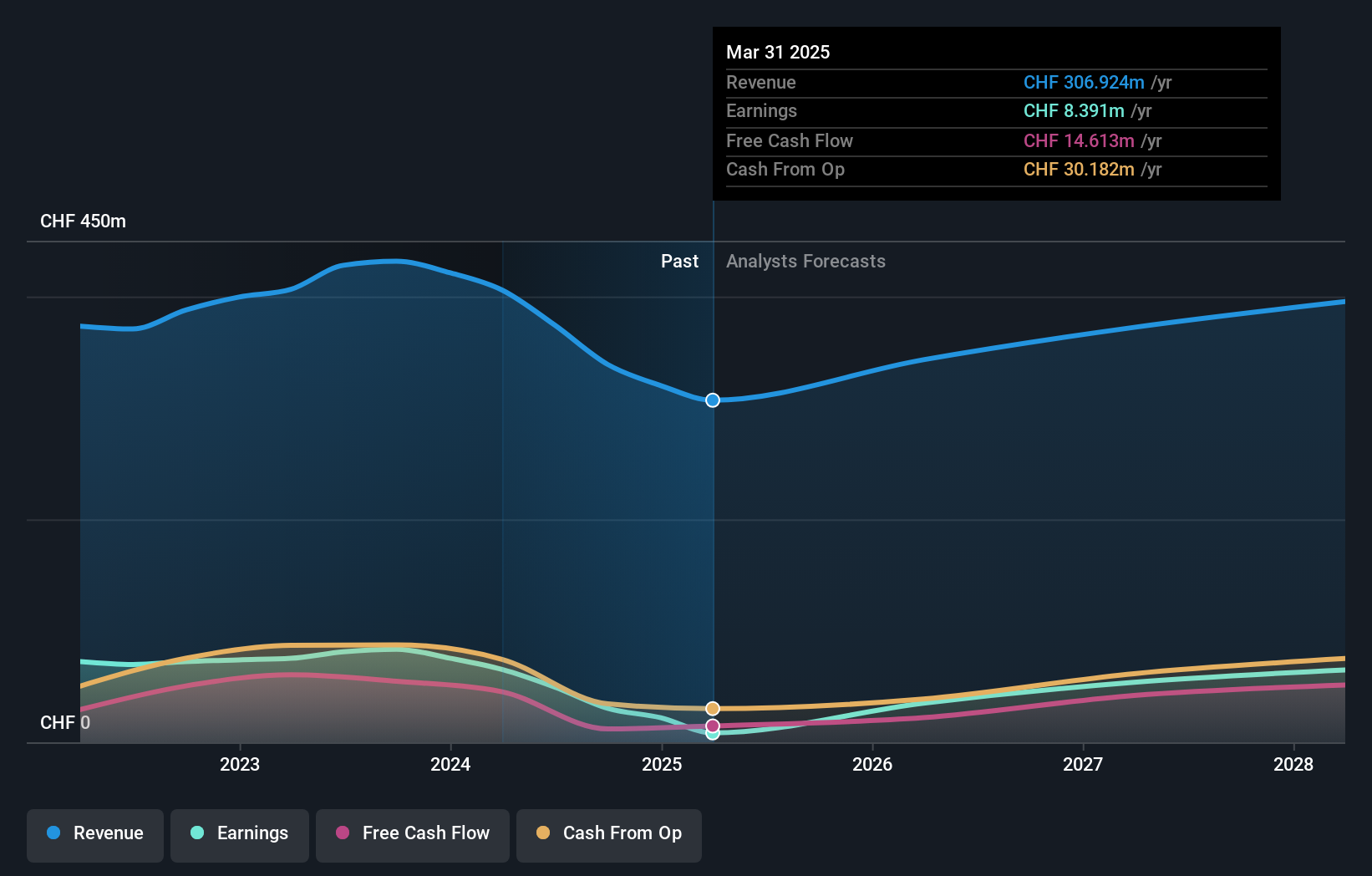

Simply Wall St Growth Rating: ★★★★☆☆

Overview: LEM Holding SA, along with its subsidiaries, offers solutions for measuring electrical parameters across various regions including China, Japan, South Korea, India, Southeast Asia, Europe, the Middle East, Africa, NAFTA and Latin America and has a market cap of CHF1.50 billion.

Operations: LEM Holding SA specializes in providing electrical parameter measurement solutions across multiple global regions. The company generates revenue by selling its products and services to various industries, with significant contributions from markets such as China, Japan, and Europe.

LEM Holding SA, a prominent Swiss tech firm, reported a significant drop in first-quarter sales to CHF 80.96 million from CHF 112.34 million last year, with net income falling to CHF 4.78 million from CHF 20.54 million. Despite this setback, the company’s earnings are projected to grow at an impressive rate of 18.4% annually over the next few years, outpacing the Swiss market’s average growth of 11.7%. LEM’s commitment to innovation is evident through its substantial R&D expenses, which have consistently been around €120 million annually (2-3% of revenue), driving advancements in their core segments like industrial automation and energy management systems.

Simply Wall St Growth Rating: ★★★★☆☆

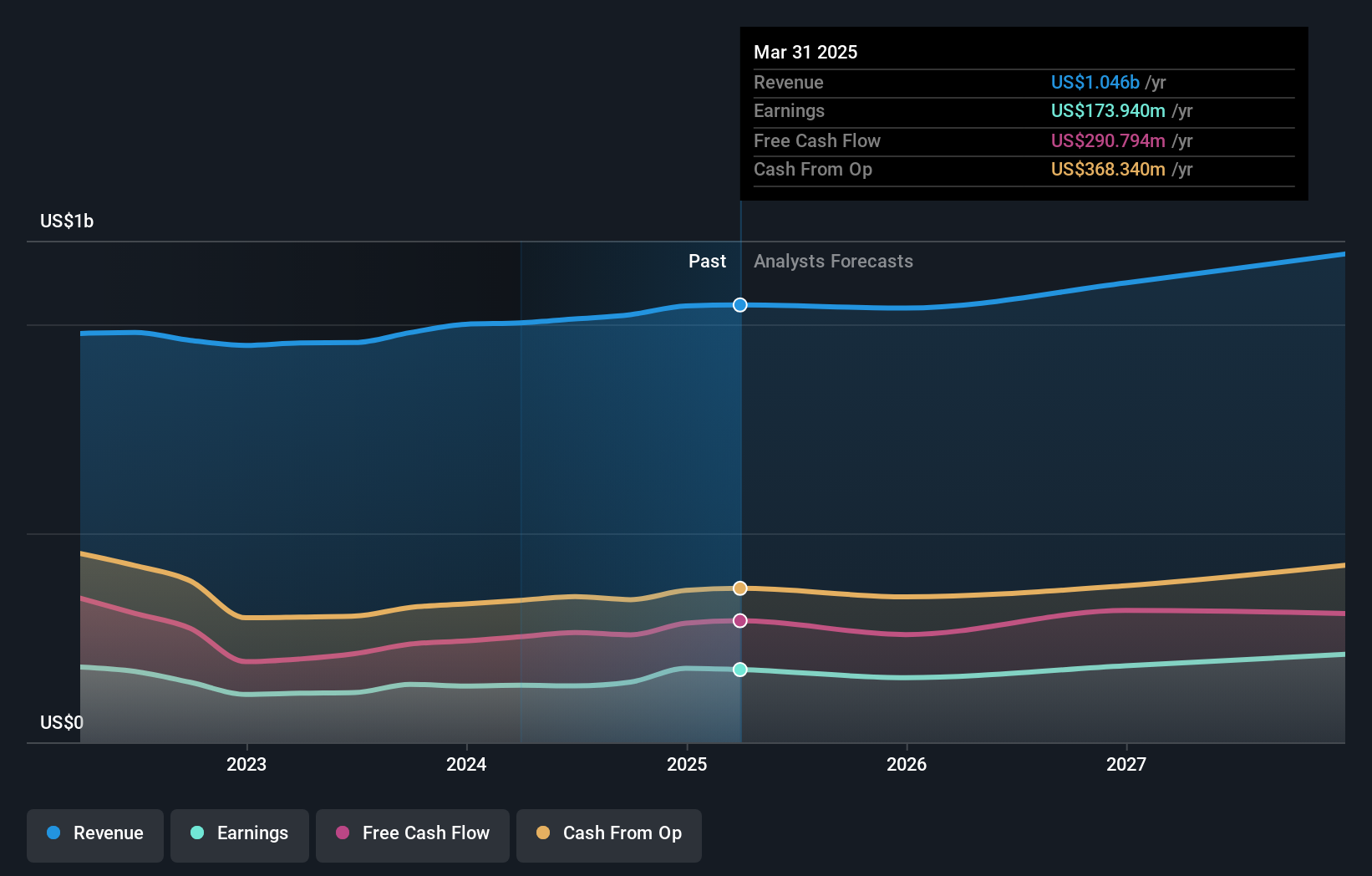

Overview: Temenos AG develops, markets, and sells integrated banking software systems to financial institutions globally, with a market cap of CHF4.45 billion.

Operations: Temenos AG specializes in providing integrated banking software systems to financial institutions worldwide. The company generates revenue primarily through the sale of its software products and related services.

Temenos, a Swiss software firm, is poised for growth with earnings expected to rise 14.3% annually, outpacing the Swiss market’s 11.7%. The firm’s revenue is projected to increase by 7.6% per year, driven by its SaaS model which ensures recurring income from subscriptions. Recent buybacks totaling CHF 200 million (4.45% of shares) reflect confidence in future prospects. Notably, Temenos’ R&D expenses have consistently been significant, underscoring its commitment to innovation and maintaining competitive edge in the software industry.

Where To Now?

Looking For Alternative Opportunities?

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we’re here to simplify it.

Discover if Temenos might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com